You aren’t even googling before making shit up now.

Dude. You are clearly not understanding me. My statement - that you specifically quoted above - summarizes each and every point your link makes. You act like you’re disagreeing with me, but you’re supporting points I’ve already made. The disagreement you are having on this issue is entirely within your own head.

For example, from your link:

If the IRS believes you have erroneously claimed a home office or other deduction, it can ding you for anywhere between $500 and $5,000. This penalty can jump to 75% if the taxpayer deliberately and fraudulently attempts to reduce their tax liability.

My previous statement (Emphasis added):

They may not allow you to claim it as a business expense, but they can’t argue fraud unless you used it for personal use despite claiming business. So don’t do that. Don’t use it for personal use when you claim it as a business use.

Your link is just quantifying the penalties for ignoring my advice. Don’t “erroneously claim a home office or other deduction”. Go ahead and claim them, just make sure your claim isn’t erroneous. You are perfectly entitled to make a valid claim.

I’m entering this from the assumption that you are steering the argument into something completely unrelated because you were proven wrong.

That might just be a piss-poor assumption. You should probably go back and see if that assumption is actually justified. (Narrator: It wasn’t.)

IT DOESN’T MATTER IF YOU CAN LEGALLY DODGE TAXES BY RUNNING A BUSINESS. THE OP STATED THAT W2 EMPLOYEES DON’T GET THE DEDUCTIONS OF A BUSINESS.

This would only be a valid statement if “being a W2 employee” precluded the individual from also running their own business. As the employee is not precluded from running a business, the W2 employee can get the deductions of running a business. You have no grounds to say that they can’t get the deductions of a business, when they can, in fact, get the deductions of a business simply by operating as a business.

Perhaps it would be useful to show you that a business is not always entitled to deduct something. For example, where a business (subcontractor) is hired by another business (prime contractor) and that prime contractor provides various direct compensation to the sub, the sub cannot deduct the expense in question. The subcontractor is, effectively, an employee of the prime contractor, even though both are businesses. Expenses made by the prime cannot be deducted by the sub. Remember that.

If the prime contractor provides eye protection and other PPE to the subcontractor, the subcontractor cannot deduct that PPE as a business expense. If the prime contractor provides transportation to and from the main job site, the subcontractor cannot claim transportation costs.

When you cannot claim your commute costs as a W2 employee, it is because the IRS requires those costs to be included in your negotiated direct compensation with your employer. Your pay specifically includes compensation for your normal commute. You are “reimbursed” for your normal commute costs, and don’t get to claim them yourself.

As a W2 employee, you can claim transportation costs to other job sites unless you are specifically reimbursed for your travel to those other job sites. If you are reimbursed, you don’t also get to claim it. Your employer gets to claim that reimbursement as a deductible expense.

If you don’t like that, don’t work as a W2 employee. Work as a contractor: a business. A contractor is allowed to deduct the expense of all non-reimbursed transportation costs, and is not expected or required to demand explicit reimbursement for transportation or other expenses in their negotiated fee.

Fraud can be overstated deductions. Given that you aren’t allowed to deduct your mortgage for a garage sale, and you are doing it every year to offset your W2 earnings, the amount of your phony deduction could be considered fraud. You can’t deduct hobby expenses.

If you don’t like that, don’t work as a W2 employee

That’s not the discussion and you know it.

“Rent is high” you: “buy a house”

“Police are corrupt” you: “become a policeman”

“Tax policy is unfair” you: “start a successful business”

you claimed you could deduct part of your mortgage for a garage sale.

I claimed that a garage sale was a business activity. I said if you didn’t think an annual garage sale was sufficient to count as a “business”, you could engage in online retailing or other additional activities as well.

You absolutely are allowed to deduct the costs for that part of your home you use exclusively for business purposes. Right from your own link:

"Part 1—Part of Your Home Used for Business

Lines 1–3.

If you figure the percentage based on area, use lines 1 through 3 to figure the business-use percentage. Enter the percentage on line 3.

You can use any other reasonable method that accurately reflects your business-use percentage. If you operate a daycare facility and you meet the exception to the exclusive use test for part or all of the area you use for business, you must figure the business-use percentage for that area as explained under Daycare Facility, earlier. If you use another method to figure your business percentage, skip lines 1 and 2 and enter the percentage on line 3.

I’m beginning to get offended at the repeated insinuations that I am advocating fraud. You are looking at BUSINESS ACTIVITIES and declaring them to be fraud. You’ve adopted some sort of weird victim mentality here. You think that if “businesses” do it, it’s permitted by the government, but if you do the exact same thing, it’s fraud. It’s not.

Have you ever worked as a 1099 contractor? Have you ever had any income whatsoever that didn’t come from a W2 or capital gains? It really doesn’t seem like it. Your position on what constitutes a “business” seems to be some kind of megacorporation, rather than a sole proprietorship. You seem to be under the impression that unless you can survive off the income of your business, it’s not a business at all.

Fraud can be overstated deductions.

I never suggested overstating deductions. Your argument here is bordering on libelous.

Given that you aren’t allowed to deduct your mortgage for a garage sale,

Your own link says otherwise.

the amount of your phony deduction could be considered fraud.

There was no phony deduction.

You can’t deduct hobby expenses.

True, but I never suggested a hobby. I suggested a business. And I described numerous activities - not just a garage sale - that would constitute business. You consistently ignore the remainder of my argument: if you don’t think a garage sale is sufficient to constitute a “business”, you can engage in online retailing and other activities as well.

“Rent is high” you: “buy a house” “Police are corrupt” you: “become a policeman” “Tax policy is unfair” you: “start a successful business”

Your first two points don’t arise from any of my arguments. As for the third, I never said “start a successful business”. I’ve said repeatedly that 30% of home businesses never show a profit. They still get to deduct their expenses. Your third observation would be better stated as “Businesses get unfair tax breaks” : “Start a business, so you an claim the same tax breaks”

That’s not the discussion and you know it.

Actually, it is the entire discussion. The fact that the IRS requires your regular commute and other expenses to be included in your negotiated pay as a W2 employee means that your expenses are effectively considered “reimbursed”. Businesses don’t get to claim reimbursed expenses as deductions. If you don’t want to include such expenses in your regular pay, you can work as a 1099 contractor rather than a W2 employee.

I claimed that a garage sale was a business activity.

You can’t deduct housing for a garage sale as you claimed.

The fact that the IRS requires your regular commute and other expenses to be included in your negotiated pay as a W2 employee means that your expenses are effectively considered “reimbursed”.

They specifically say you can’t deduct even if the employer doesn’t reimburse.

“Employees can’t deduct this cost even if their employer doesn’t reimburse the employee for using their own car.”

You can’t deduct housing for a garage sale as you claimed.

Your own link says that I can, especially when you get around to acknowledging that the garage sale was just one small business activity of the whole business I described. I included “online retail” as an additional business activity specifically because I thought you would have a problem with the garage sale alone. I’ve already addressed your “garage sale” concerns; I addressed them before you raised them. Your own link says I can deduct from my housing costs the percentage of the house I use for business purposes. It specifically says I can use any “reasonable method that accurately reflects your business-use percentage” to make that determination.

They specifically say you can’t deduct even if the employer doesn’t reimburse.

The IRS basically acts as though your regular pay specifically includes reimbursement for your regular commute. Your regular commute is already paid for with your pay, which is why you can’t claim it. The pay you negotiate with your W2 employer already includes (but does not specifically itemize) reimbursement for your regular commute. That is why you don’t get to separately deduct it.

Your regular pay does not cover atypical travel. If you are temporarily forced to drive 5 miles further to a different job site, you can claim that additional 5 miles. Compensation for that additional mileage is not included in your regular pay. If that additional mileage is not specifically reimbursed, you can claim it, even as a W2 employee.

Companies do not offer that choice to everyone.

Then find a different company. Find three, or ten. You’re a contractor: you provide a contracted service, not your time. You provide it to anyone you want, not just a single company. That’s what it means to be a contractor, rather than an employee. You have the flexibility in defining exactly what business you will be doing. You don’t have to fit the narrow IRS restrictions associated with W2 employment. You operate as a business, and you are taxed as a business.

especially when you get around to acknowledging that the garage sale was just one small business activity of the whole business I described.

Read what you wrote:

"Forget all of that, hold an annual garage sale.

Now, you’re a business. You get to deduct the poster board you purchase advertising your sale. You get to deduct the balloons and price stickers.

You also get to deduct that part of your rent or mortgage that you spend on the garage where you keep your inventory. That is now your “warehouse”, which is part of your (non-employment) business. How about your attic? The attic is part of your home. You pay mortgage/rent/taxes on that part of your home right along with every other part. I doubt you use it for anything but storage anyway. Put the crap in your attic on your lawn with a price tag once a year, and you get to deduct the part of your housing payment that goes toward your attic.

You get to deduct the cost of acquiring your inventory. That is also a business expense.

Spend an afternoon in a lawnchair while your neighbors look through your junk inventory, and you get to claim thousands of dollars in business expenses.

If you’re worried the IRS might take issue with you if you only do this once a year, you can put up an ebay, etsy, craigslist, or marketplace listing, and it becomes a year-round operation."

You posted what the IRS could classify as fraud and then added “If you are worried…” as an addendum.

Creating an ebay account does not allow you to deduct your rent. You need to sell regularly as a business to qualify. Only the portion of the space used exclusively for business is deductible.

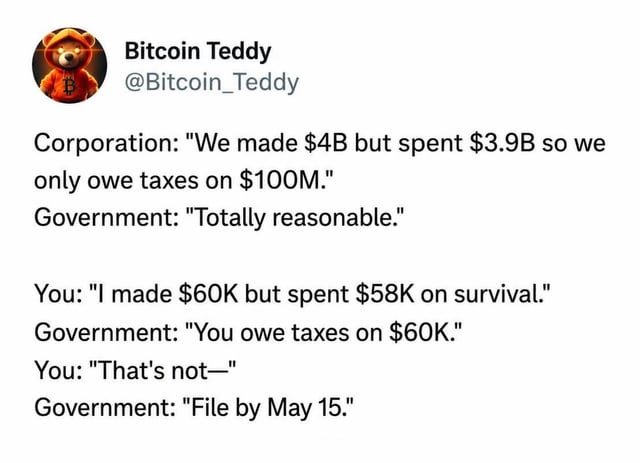

So we have everything that isn’t profit for a business is taxed vs everything that isn’t business related for a taxpayer is taxed. It hasn’t changed the OP’s statement at all. If a business needs an office to operate its completely tax deductible but the bedroom of your house where you need to sleep isn’t tax deductible.

The IRS basically acts as though your regular pay s

“Acts” is your opinion. I specifically quoted the IRS publication where they said that isn’t true.

The pay you negotiate with your W2 employer already includes

The IRS said they specifically do not consider it is included.

Then find a different company.

People are forced through from their birth lottery (intelligence and family wealth) into a system that dictates the rules. Finding the perfect job is often impossible because the choice isn’t there.

You posted what the IRS could classify as fraud and then added “If you are worried…” as an addendum.

You claim they could. Not them. They would be burdened with proving it beyond a shadow of a doubt. Which they can’t do, because you can cite their explicit guidance to support your claim of business use. It’s not fraud, because they specifically state that you can claim everything I said. You linked the exact statement that allows it, and I’ve cited it earlier. The “addendum” I added was for your benefit, because I recognized that the “garage sale” example was probably too foreign a concept for you to rationally consider. But yes, if 50% of my home is used exclusively for business 1 day a year, I can deduct 1/365 * 50% * annual rent of my home. If I use a room that is 10% of the floor space of my home exclusively to store and handle merchandise for my online storefront, I can deduct 10% of my rent.

Creating an ebay account does not allow you to deduct your rent. You need to sell regularly as a business to qualify.

You need to regularly offer for sale.

If a business needs an office to operate its completely tax deductible but the bedroom of your house where you need to sleep isn’t tax deductible.

Correct. You’re restating what I said in my initial comment: “You also get to deduct that part of your rent or mortgage that you spend on the garage where you keep your inventory.” You’re repeating my words back to me, after declaring my words to be fraud.

“Acts” is your opinion. I specifically quoted the IRS publication where they said that isn’t true.

That citation does not apply to the circumstances we are discussing here.

The IRS said they specifically do not consider it is included.

This entire discussion is predicated on the fact that they do not allow deductions for things like commuting, when they do allow deductions for 1099 contractors to travel to job sites, and they do allow W2 employees to deduct travel to places other than their normal place of work. They do not allow these deductions where the travel costs are reimbursed, whether for W2 employees or for 1099 contractors. So, regular commuting is not deductible; reimbursed travel is not deductible. Regular commuting is treated the same way as reimbursed travel. Contrary to what you think you read, the IRS does treat normal commutes as reimbursed travel.

People are forced through from their birth lottery (intelligence and family wealth) into a system that dictates the rules.

Horseshit. Pure, unadulterated horseshit. There are millions of 1099 workers in the economy. If this tax issue is sufficiently important, you will join them. If it’s not important enough to do something effective, you can try to achieve some sort of change through the political process.

Finding the perfect job is often impossible because the choice isn’t there.

In this discussion, you have repeatedly and consistently misidentified perfectly legitimate business practices as “fraud”. You have repeatedly defamed me for promoting these perfectly legitimate business practices by declaring them fraud.

You now argue that you don’t have the “choice” of your perfect job.

Your perceptions are the problem here. You are failing to recognize the wide variety of choice that you do have. The constraints of “fraud” aren’t where you think they are. You are allowed to do far more than what you think you can do. This “lack of choice” problem is entirely within your own head. You are rejecting good options because you don’t understand that they are good. You are mistaking them for fraud, then claiming you don’t have them.

If it’s not important enough to do something effective, you can try to achieve some sort of change through the political process.

And you have constantly refused to acknowledge that the tax laws aren’t consistent.

Your equivalent position: “Police brutality isnt a problem, become a policeman so you are above the law or change it with politics.”

I’ve been on all sides. I’ve been W2. I’ve been W2 with a side business. I’ve been president of a large ISP. I don’t have to be in the fight to see injustice.

And you have constantly refused to acknowledge that the tax laws aren’t consistent.

I’ve shown the consistency.

A W2 worker is, effectively, a subcontractor to a prime contractor who reimburses all normal work expenses. The subcontractor doesn’t get to deduct their travel expenses, because they are part of the normal compensation. The subcontractor doesn’t get to deduct PPE, because they are provided by the prime. The subcontractor doesn’t get to deduct clothing or laundry or tools, because all of those are provided (or reimbursed) by the prime. This arrangement between the prime and the subcontractor is functionally identical to that of the prime with a W2 employee.

The subcontractor does get to deduct atypical expenses not included in the normal, negotiated pay. So does the W2 employee.

The term for the comparison between “W2 Worker” and the type of subcontractor I described is “consistent”. They are able to make the same deductions for the same reasons. They are taxed the same. A W2 worker is a subcontractor whose normal expenditures are all reimbursed by the prime. The distinction between them has no relevant difference.

The tax scheme for a W2 employee is simplified relative to that of a 1099 worker. This is the sine qua non of W2 employment. This simplification is the explicit reason why this category exists. This category of worker incorporates all “normal” expenditures, making all of them the responsibility of the employer, and included in “normal”, negotiated pay. These “normal”, routine, recurring expenditures don’t need to be explicitly itemized on the tax return. They are already treated as reimbursed through regular pay, so they are already incorporated and not subject to deduction. The need for these expenditures is included in your pay negotiation with your employer.

This simplification does not extend to abnormal or atypical expenses incurred by the worker. Where the W2 worker incurs abnormal or atypical, non-reimbursed expenses, they can, indeed, claim these expenses. Only normal, recurring expenses are included in the pay negotiated with the employer.

What you are trying to achieve is something that already exists in the tax code. Colloquially, it’s called the “1099 Worker”. We already have the “1099 Worker”. You’re trying to reinvent the “1099 Worker”. But we already have the “1099 Worker”. Everything you are trying to achieve for the W2 employee is already present in the “1099 Worker” category. If you want the benefits of a “1099 Worker”, go ahead and become a “1099 Worker”. You can certainly hire yourself out to one or more businesses as a “1099 Worker”. Companies hire “1099 Workers” all the time for specific purposes. Yes, the overwhelming majority of jobs are filled by W2 employees, but certainly not all. There is plenty of opportunity for you to operate as a “1099 Worker” if your specific needs aren’t being met by W2 employment.

{kind=link}

Dude. You are clearly not understanding me. My statement - that you specifically quoted above - summarizes each and every point your link makes. You act like you’re disagreeing with me, but you’re supporting points I’ve already made. The disagreement you are having on this issue is entirely within your own head.

For example, from your link:

My previous statement (Emphasis added):

Your link is just quantifying the penalties for ignoring my advice. Don’t “erroneously claim a home office or other deduction”. Go ahead and claim them, just make sure your claim isn’t erroneous. You are perfectly entitled to make a valid claim.

That might just be a piss-poor assumption. You should probably go back and see if that assumption is actually justified. (Narrator: It wasn’t.)

This would only be a valid statement if “being a W2 employee” precluded the individual from also running their own business. As the employee is not precluded from running a business, the W2 employee can get the deductions of running a business. You have no grounds to say that they can’t get the deductions of a business, when they can, in fact, get the deductions of a business simply by operating as a business.

Perhaps it would be useful to show you that a business is not always entitled to deduct something. For example, where a business (subcontractor) is hired by another business (prime contractor) and that prime contractor provides various direct compensation to the sub, the sub cannot deduct the expense in question. The subcontractor is, effectively, an employee of the prime contractor, even though both are businesses. Expenses made by the prime cannot be deducted by the sub. Remember that.

If the prime contractor provides eye protection and other PPE to the subcontractor, the subcontractor cannot deduct that PPE as a business expense. If the prime contractor provides transportation to and from the main job site, the subcontractor cannot claim transportation costs.

When you cannot claim your commute costs as a W2 employee, it is because the IRS requires those costs to be included in your negotiated direct compensation with your employer. Your pay specifically includes compensation for your normal commute. You are “reimbursed” for your normal commute costs, and don’t get to claim them yourself.

As a W2 employee, you can claim transportation costs to other job sites unless you are specifically reimbursed for your travel to those other job sites. If you are reimbursed, you don’t also get to claim it. Your employer gets to claim that reimbursement as a deductible expense.

If you don’t like that, don’t work as a W2 employee. Work as a contractor: a business. A contractor is allowed to deduct the expense of all non-reimbursed transportation costs, and is not expected or required to demand explicit reimbursement for transportation or other expenses in their negotiated fee.

you claimed you could deduct part of your mortgage for a garage sale.

You claimed it isn’t fraud if you can show the source.

You aren’t allowed to deduct your mortgage for a garage sale.

https://www.irs.gov/publications/p587

Fraud can be overstated deductions. Given that you aren’t allowed to deduct your mortgage for a garage sale, and you are doing it every year to offset your W2 earnings, the amount of your phony deduction could be considered fraud. You can’t deduct hobby expenses.

That’s not the discussion and you know it.

“Rent is high” you: “buy a house” “Police are corrupt” you: “become a policeman” “Tax policy is unfair” you: “start a successful business”

I claimed that a garage sale was a business activity. I said if you didn’t think an annual garage sale was sufficient to count as a “business”, you could engage in online retailing or other additional activities as well.

You absolutely are allowed to deduct the costs for that part of your home you use exclusively for business purposes. Right from your own link:

I’m beginning to get offended at the repeated insinuations that I am advocating fraud. You are looking at BUSINESS ACTIVITIES and declaring them to be fraud. You’ve adopted some sort of weird victim mentality here. You think that if “businesses” do it, it’s permitted by the government, but if you do the exact same thing, it’s fraud. It’s not.

Have you ever worked as a 1099 contractor? Have you ever had any income whatsoever that didn’t come from a W2 or capital gains? It really doesn’t seem like it. Your position on what constitutes a “business” seems to be some kind of megacorporation, rather than a sole proprietorship. You seem to be under the impression that unless you can survive off the income of your business, it’s not a business at all.

I never suggested overstating deductions. Your argument here is bordering on libelous.

Your own link says otherwise.

There was no phony deduction.

True, but I never suggested a hobby. I suggested a business. And I described numerous activities - not just a garage sale - that would constitute business. You consistently ignore the remainder of my argument: if you don’t think a garage sale is sufficient to constitute a “business”, you can engage in online retailing and other activities as well.

Your first two points don’t arise from any of my arguments. As for the third, I never said “start a successful business”. I’ve said repeatedly that 30% of home businesses never show a profit. They still get to deduct their expenses. Your third observation would be better stated as “Businesses get unfair tax breaks” : “Start a business, so you an claim the same tax breaks”

Actually, it is the entire discussion. The fact that the IRS requires your regular commute and other expenses to be included in your negotiated pay as a W2 employee means that your expenses are effectively considered “reimbursed”. Businesses don’t get to claim reimbursed expenses as deductions. If you don’t want to include such expenses in your regular pay, you can work as a 1099 contractor rather than a W2 employee.

You can’t deduct housing for a garage sale as you claimed.

They specifically say you can’t deduct even if the employer doesn’t reimburse.

“Employees can’t deduct this cost even if their employer doesn’t reimburse the employee for using their own car.”

https://www.irs.gov/newsroom/heres-the-411-on-who-can-deduct-car-expenses-on-their-tax-returns

So the IRS does not consider your salary as including reimbursement for transportation.

“you can work as a 1099 contractor rather than a W2 employee.”

Companies do not offer that choice to everyone.

Your own link says that I can, especially when you get around to acknowledging that the garage sale was just one small business activity of the whole business I described. I included “online retail” as an additional business activity specifically because I thought you would have a problem with the garage sale alone. I’ve already addressed your “garage sale” concerns; I addressed them before you raised them. Your own link says I can deduct from my housing costs the percentage of the house I use for business purposes. It specifically says I can use any “reasonable method that accurately reflects your business-use percentage” to make that determination.

The IRS basically acts as though your regular pay specifically includes reimbursement for your regular commute. Your regular commute is already paid for with your pay, which is why you can’t claim it. The pay you negotiate with your W2 employer already includes (but does not specifically itemize) reimbursement for your regular commute. That is why you don’t get to separately deduct it.

Your regular pay does not cover atypical travel. If you are temporarily forced to drive 5 miles further to a different job site, you can claim that additional 5 miles. Compensation for that additional mileage is not included in your regular pay. If that additional mileage is not specifically reimbursed, you can claim it, even as a W2 employee.

Then find a different company. Find three, or ten. You’re a contractor: you provide a contracted service, not your time. You provide it to anyone you want, not just a single company. That’s what it means to be a contractor, rather than an employee. You have the flexibility in defining exactly what business you will be doing. You don’t have to fit the narrow IRS restrictions associated with W2 employment. You operate as a business, and you are taxed as a business.

Read what you wrote:

You posted what the IRS could classify as fraud and then added “If you are worried…” as an addendum.

Creating an ebay account does not allow you to deduct your rent. You need to sell regularly as a business to qualify. Only the portion of the space used exclusively for business is deductible.

So we have everything that isn’t profit for a business is taxed vs everything that isn’t business related for a taxpayer is taxed. It hasn’t changed the OP’s statement at all. If a business needs an office to operate its completely tax deductible but the bedroom of your house where you need to sleep isn’t tax deductible.

“Acts” is your opinion. I specifically quoted the IRS publication where they said that isn’t true.

The IRS said they specifically do not consider it is included.

People are forced through from their birth lottery (intelligence and family wealth) into a system that dictates the rules. Finding the perfect job is often impossible because the choice isn’t there.

You claim they could. Not them. They would be burdened with proving it beyond a shadow of a doubt. Which they can’t do, because you can cite their explicit guidance to support your claim of business use. It’s not fraud, because they specifically state that you can claim everything I said. You linked the exact statement that allows it, and I’ve cited it earlier. The “addendum” I added was for your benefit, because I recognized that the “garage sale” example was probably too foreign a concept for you to rationally consider. But yes, if 50% of my home is used exclusively for business 1 day a year, I can deduct 1/365 * 50% * annual rent of my home. If I use a room that is 10% of the floor space of my home exclusively to store and handle merchandise for my online storefront, I can deduct 10% of my rent.

You need to regularly offer for sale.

Correct. You’re restating what I said in my initial comment: “You also get to deduct that part of your rent or mortgage that you spend on the garage where you keep your inventory.” You’re repeating my words back to me, after declaring my words to be fraud.

That citation does not apply to the circumstances we are discussing here.

This entire discussion is predicated on the fact that they do not allow deductions for things like commuting, when they do allow deductions for 1099 contractors to travel to job sites, and they do allow W2 employees to deduct travel to places other than their normal place of work. They do not allow these deductions where the travel costs are reimbursed, whether for W2 employees or for 1099 contractors. So, regular commuting is not deductible; reimbursed travel is not deductible. Regular commuting is treated the same way as reimbursed travel. Contrary to what you think you read, the IRS does treat normal commutes as reimbursed travel.

Horseshit. Pure, unadulterated horseshit. There are millions of 1099 workers in the economy. If this tax issue is sufficiently important, you will join them. If it’s not important enough to do something effective, you can try to achieve some sort of change through the political process.

In this discussion, you have repeatedly and consistently misidentified perfectly legitimate business practices as “fraud”. You have repeatedly defamed me for promoting these perfectly legitimate business practices by declaring them fraud.

You now argue that you don’t have the “choice” of your perfect job.

Your perceptions are the problem here. You are failing to recognize the wide variety of choice that you do have. The constraints of “fraud” aren’t where you think they are. You are allowed to do far more than what you think you can do. This “lack of choice” problem is entirely within your own head. You are rejecting good options because you don’t understand that they are good. You are mistaking them for fraud, then claiming you don’t have them.

Be the choice.

And you have constantly refused to acknowledge that the tax laws aren’t consistent.

Your equivalent position: “Police brutality isnt a problem, become a policeman so you are above the law or change it with politics.”

I’ve been on all sides. I’ve been W2. I’ve been W2 with a side business. I’ve been president of a large ISP. I don’t have to be in the fight to see injustice.

I’ve shown the consistency.

A W2 worker is, effectively, a subcontractor to a prime contractor who reimburses all normal work expenses. The subcontractor doesn’t get to deduct their travel expenses, because they are part of the normal compensation. The subcontractor doesn’t get to deduct PPE, because they are provided by the prime. The subcontractor doesn’t get to deduct clothing or laundry or tools, because all of those are provided (or reimbursed) by the prime. This arrangement between the prime and the subcontractor is functionally identical to that of the prime with a W2 employee.

The subcontractor does get to deduct atypical expenses not included in the normal, negotiated pay. So does the W2 employee.

The term for the comparison between “W2 Worker” and the type of subcontractor I described is “consistent”. They are able to make the same deductions for the same reasons. They are taxed the same. A W2 worker is a subcontractor whose normal expenditures are all reimbursed by the prime. The distinction between them has no relevant difference.

The tax scheme for a W2 employee is simplified relative to that of a 1099 worker. This is the sine qua non of W2 employment. This simplification is the explicit reason why this category exists. This category of worker incorporates all “normal” expenditures, making all of them the responsibility of the employer, and included in “normal”, negotiated pay. These “normal”, routine, recurring expenditures don’t need to be explicitly itemized on the tax return. They are already treated as reimbursed through regular pay, so they are already incorporated and not subject to deduction. The need for these expenditures is included in your pay negotiation with your employer.

This simplification does not extend to abnormal or atypical expenses incurred by the worker. Where the W2 worker incurs abnormal or atypical, non-reimbursed expenses, they can, indeed, claim these expenses. Only normal, recurring expenses are included in the pay negotiated with the employer.

What you are trying to achieve is something that already exists in the tax code. Colloquially, it’s called the “1099 Worker”. We already have the “1099 Worker”. You’re trying to reinvent the “1099 Worker”. But we already have the “1099 Worker”. Everything you are trying to achieve for the W2 employee is already present in the “1099 Worker” category. If you want the benefits of a “1099 Worker”, go ahead and become a “1099 Worker”. You can certainly hire yourself out to one or more businesses as a “1099 Worker”. Companies hire “1099 Workers” all the time for specific purposes. Yes, the overwhelming majority of jobs are filled by W2 employees, but certainly not all. There is plenty of opportunity for you to operate as a “1099 Worker” if your specific needs aren’t being met by W2 employment.